Money is not just about earning, it’s about keeping it. Inflation and currency depreciation are silent destroyers of wealth. You can work for decades, save diligently, and still find your purchasing power diminished if you store money in the wrong place.

That raises an important question: Which is the best country to park your money? Looking back over the past decade (2015–2025), the answer lies in a combination of low inflation and strong or stable currencies.

Why Safe Havens Matter

When you keep money in local currency, two forces determine how much of it survives:

- Inflation: Prices rising year after year.

- Exchange rates: How your currency performs against global benchmarks like the U.S. dollar.

If inflation runs high or your currency weakens, your wealth silently drains away. On the other hand, if both are stable, your money retains power.

This is why choosing where to hold wealth is just as important as how you earn it.

The Safe Havens: Top 10 Countries

Based on USD-adjusted erosion from 2015 to 2025, these countries stand out as the most resilient places to store cash.

1. Switzerland (CHF)

Low inflation and a franc that appreciated against the U.S. dollar. Swiss stability remains unmatched.

2. Hong Kong (HKD)

Currency pegged tightly to the USD (7.75–7.85 range). Combined with low inflation, this peg has kept wealth secure for decades.

3. Singapore (SGD)

Disciplined monetary policy and a currency that stayed flat to slightly stronger against the dollar. Reliable, resilient, and internationally trusted.

4. United States (USD)

Holding dollars means no FX risk for USD-based investors. Inflation spiked in 2021–2023, but the dollar’s global dominance helped it outperform many peers.

5. Saudi Arabia (SAR)

Pegged to the dollar at ~3.75. Moderate inflation kept real losses limited.

6. United Arab Emirates (AED)

Another long-standing peg (~3.6725) with moderate inflation. Attractive for expatriates and investors.

7. Qatar (QAR)

Stable peg at 3.64. Moderate inflation and a strong resource-backed economy.

8. Oman (OMR)

De facto peg (~1 OMR ≈ $2.60), one of the strongest units globally. Inflation remained manageable.

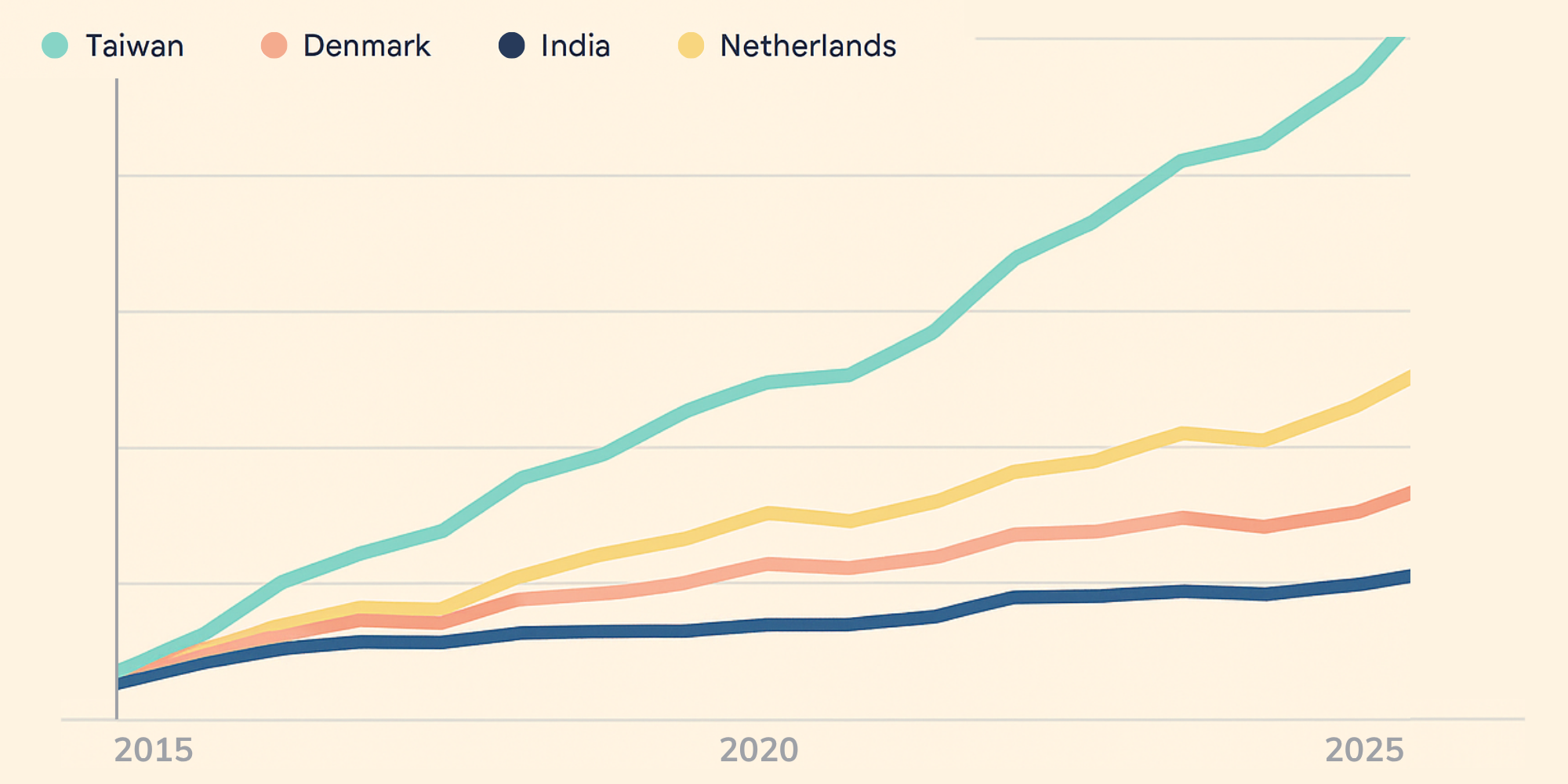

9. Taiwan (TWD)

Low inflation and a broadly range-bound currency. Taiwan’s tech leadership bolstered confidence.

10. Panama (USD)

Dollarized economy, it literally uses the U.S. dollar. Inflation stayed contained, making Panama one of the simplest safe havens.

These economies either maintained ultra-low inflation (like Switzerland and Taiwan) or pegged their currencies to the USD, neutralizing FX risk.

The Fragile Currencies: Where Wealth Evaporated

At the other end of the spectrum, several countries experienced catastrophic erosion.

- Argentina: Inflation above 200% in 2023.

- Venezuela: Hyperinflation exceeded one million percent in 2018.

- Zimbabwe: Famously saw sextillions of percent inflation; repeated currency collapses.

- Turkey (TRY): Persistent depreciation due to unconventional monetary policy.

- Myanmar, Indonesia, Laos, Guinea, Iran: Structural weaknesses or political instability crushed their currencies.

In these places, saving in local currency was a recipe for wealth destruction.

The Caveats

The top 10 list measures inflation and FX erosion. But there are other factors to consider:

- Accessibility: Some banks limit accounts for foreigners.

- Taxes: Gains may be taxed differently depending on jurisdiction.

- Capital controls: Governments can restrict withdrawals or transfers.

- Political stability: Even pegged currencies can face pressure if reserves run thin.

For example, Hong Kong’s peg has held for decades, but political uncertainty remains a long-term risk. Gulf states have defended their pegs successfully, but no peg is truly eternal.

Wealth Preservation Strategies

If you live in or are exposed to high-inflation countries, here are practical ways to protect wealth:

1. High Inflation, Not Hyperinflation (Turkey, Indonesia, etc)

- Open USD or EUR accounts if available.

- Invest abroad via ETFs or international brokerage accounts.

- Hold gold or inflation-linked bonds.

- Explore USD-pegged stablecoins (USDT, USDC) if accessible.

2. Hyperinflation (Venezuela, Zimbabwe, Argentina at risk)

- Dollarize savings informally, many locals already do this.

- Store wealth in durable goods (electronics, imported consumables).

- Hold property abroad if possible.

- Use diaspora networks and remittances to access stable currencies.

A Simplified Steps Guide: Protecting Wealth Globally

- With $1,000: Keep part in local currency for daily needs, but convert the rest into USD, gold, or stablecoins. Even small hedges matter.

- With $10,000: Diversify across 2–3 stable currencies (USD, CHF, SGD) plus a slice of real assets like gold. Use international ETFs if available.

- With $100,000: Build a multi-country safety net. International stocks, and long-term gold reserves.

The key principle: don’t let all your wealth be tied up in one unstable currency.

Closing Thought

Currencies can quietly build or destroy wealth. From Switzerland’s franc to Venezuela’s bolívar, the past decade proved that where you park your money matters as much as how you earn it.

The Wealth Waterfall philosophy emphasizes flows that survive across borders, currencies, and crises. Because true wealth isn’t just about accumulation, it’s about protection.

If you want to learn how to design resilient wealth flows that thrive no matter where you live, The Wealth Waterfall lays out the complete framework. Don’t just save, preserve.